...

...

The latest IPCC reports have painted a bleak picture of the threats our planet faces if warming isn’t limited to 1.5 °C.

Achieving this relies on immediate and drastic action from companies: through environmental transparency, ambitious emissions reduction targets, and clear transition plans.

A group of under 200 of the highest-impact publicly listed companies may account for as much as 80% of industrial emissions.[1] If we are to achieve the Paris agreement, these organizations must decarbonize at the rate climate science demands. That requires having high-quality emissions reduction targets covering all their relevant emissions that are in line with a 1.5 °C pathway.

The CDP/WWF temperature ratings methodology, which analyses corporate targets disclosed through CDP, is an insightful tool to assess the quality of targets set by these companies so far. Using this approach and looking at science-based targets (SBTs), we assessed the climate targets of 166 of the world’s highest-impact companies – finding current ambition to be far off track.

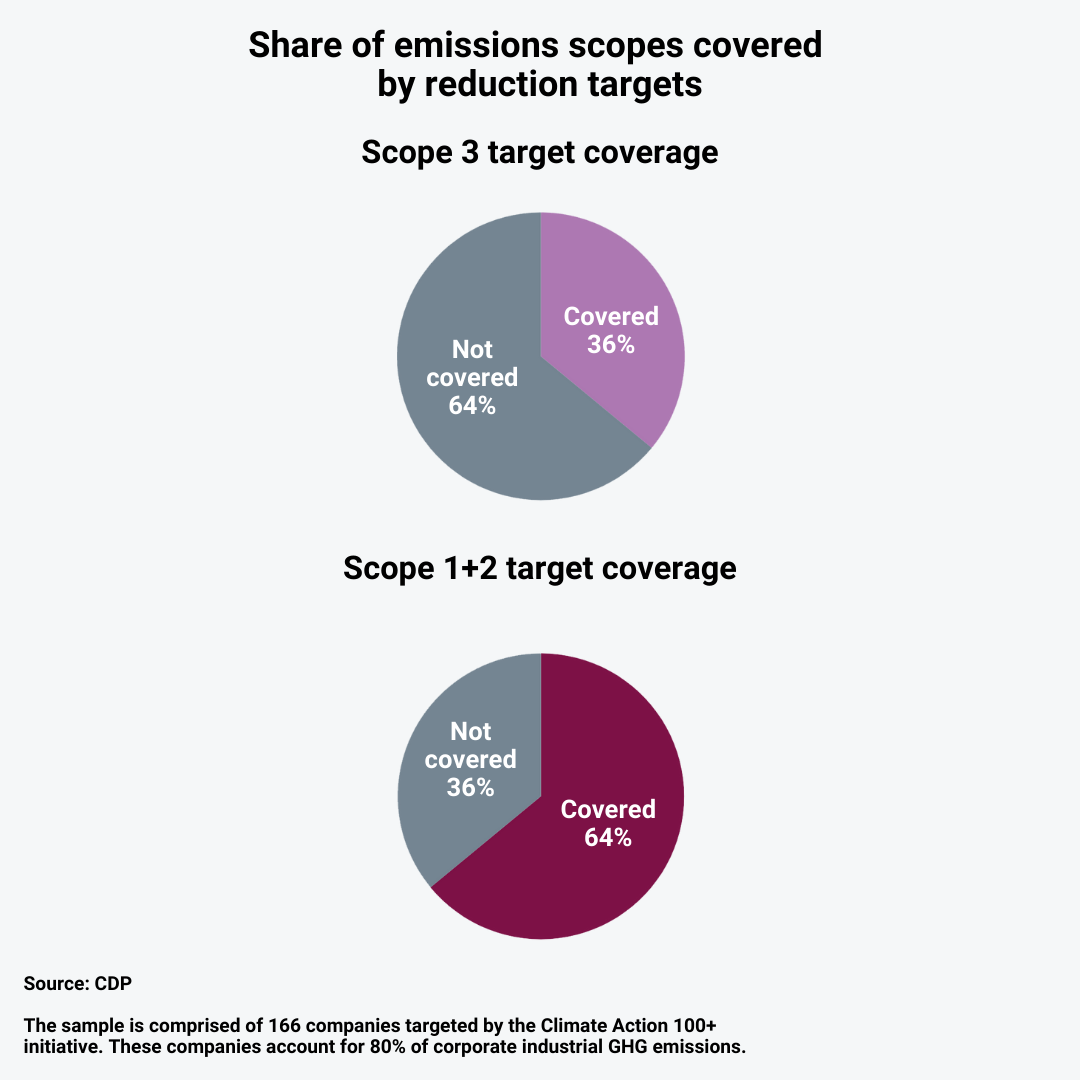

Just 36% of Scope 3 emissions are currently covered by a high-quality target

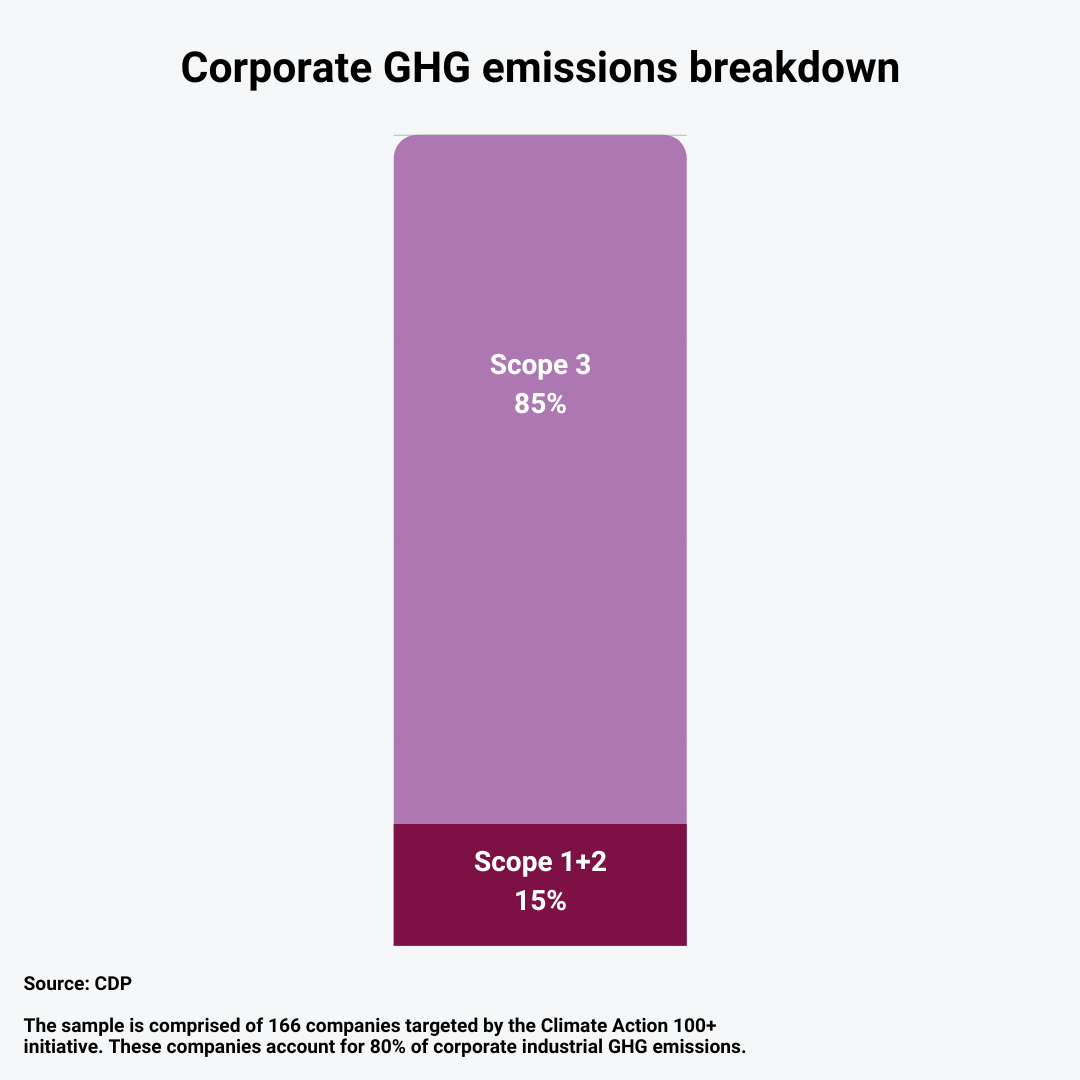

Around 85% of all corporate emissions are Scope 3, embedded within supply chains or generated during the use of products. As a result, it’s essential that high-impact companies look outside direct operations to achieve the level of decarbonization needed for 1.5 °C.

The potential impact that high-emitting companies can achieve is immense. Among the group of 166 high-impact companies we analyzed, around 27 gigatons of greenhouse gas equivalent CO2 are in these companies’ value chains.[2] That’s equivalent to around 70% of current global industrial emissions.

But our data reveal companies setting very limited targets where it matters. Just 36% of these Scope 3 emissions are currently covered by a high-quality reduction target, leaving some 17 gigatons of annual emissions without the likelihood of being reduced.

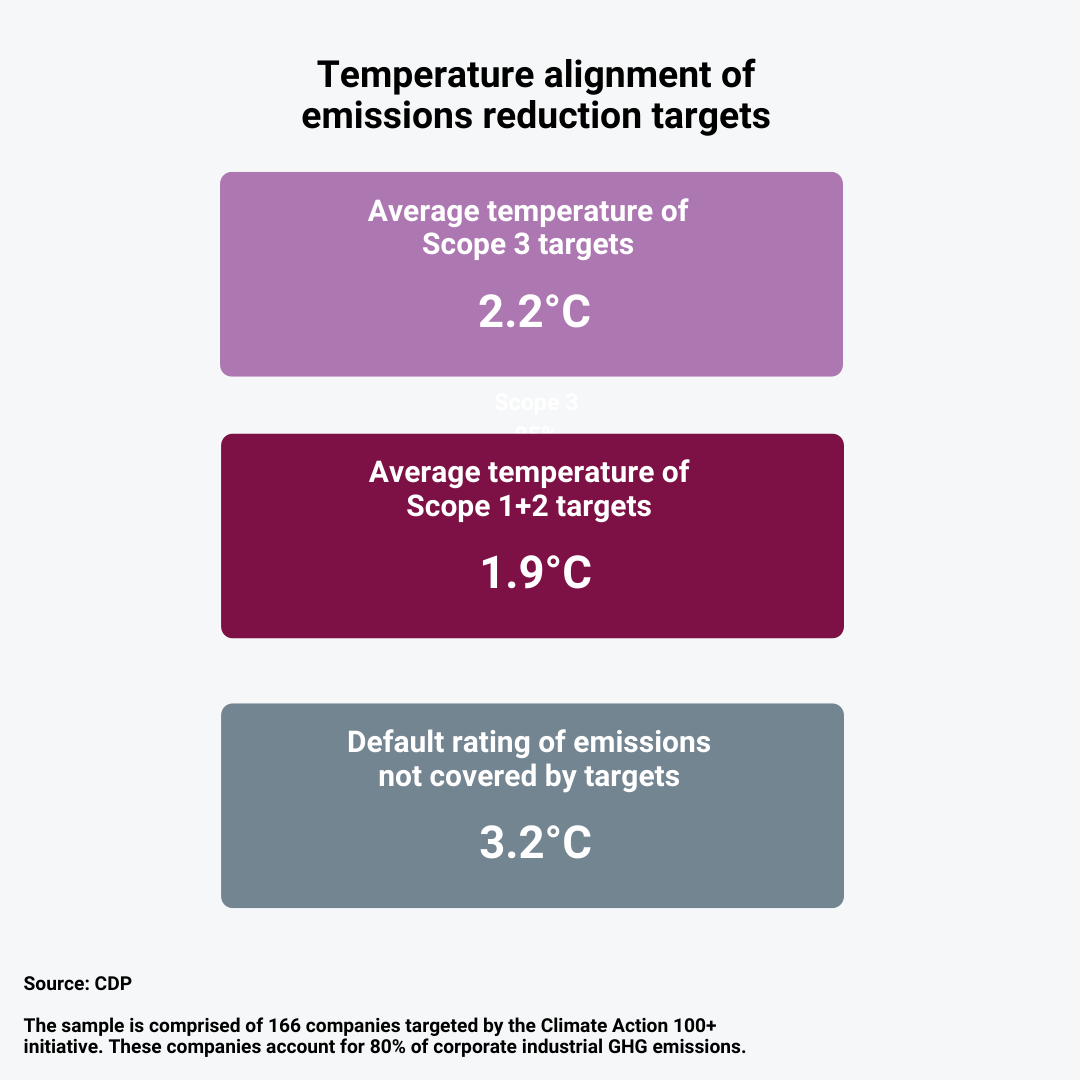

The ambition level of these targets is also too low, as our analysis estimates the ambition level to imply a 2.2 °C temperature rise.[3]

Our temperature ratings methodology considers a target to be high-quality if it defines the scope and volume (boundary) of emissions covered, and if they are short/medium-term targets that incentivize action now.

As a result, targets with a 2050 timeline are not considered high-quality, while near-term approved science-based targets are.

The lack of current ambition by the world’s most impactful companies – with enormous supply chains and customer volumes – to set high-quality targets covering their full impact poses a major risk to the likelihood of halving emissions by the end of this decade.

Many companies have targets covering their direct emissions (Scope 1 and 2), but progress on reducing these emissions is too slow

Looking at companies’ operational emissions only, our analysis shows that nearly two-thirds of emissions are now covered by a high-quality reduction target and that these targets are collectively aligned with 2 °C.

This is encouraging, though there remains a clear gap to the ambition of the Paris agreement. It shows that we may be achieving a critical mass in terms of high-impact companies acting on their direct impacts.

However, there is a long way to go, since Scope 1 and 2 represent just 15% of these companies’ emissions.

And analysis of trends in actual emissions among the high-impact group points to an average alignment of future emissions to a 2.3°C pathway. This means companies are currently off track to meet their existing targets addressing their easier-to-reach direct emissions, let alone the goals of the Paris agreement.

We must urgently see faster implementation of transition plans to deliver actual emissions reductions in line with the targets set.

High-impact companies are collectively aligned with 2.7 °C of warming

Analysing the emissions reductions targets (or lack of) disclosed by these companies, or approved by the SBTi, shows that the current ambition level falls far short of the 1.5 °C goal that the Paris agreement and IPCC science demand we achieve.

What’s positive, however, is once companies do set high-quality targets, they tend to be ambitious. When companies have set targets, the ambition level assessed has an implied temperature rise of approximately 2°C. While still far from the Paris agreement, this represents a significant difference to the 3°C scenario predicted if corporate emissions continue to rise unchecked.

This means the critical step is to ensure high-impact companies without good quality targets set them fast.

We need better targets and real reductions taking place

Put simply, it’s unlikely whether we can achieve the Paris agreement if the world’s heaviest emitters don’t set better and more ambitious GHG reduction targets material to their business.

When looking at upstream or downstream emissions, achieving the reductions needed won’t be easy. But tools exist, and the largest emitters have a responsibility to lead the way and cascade high ambition throughout the corporate world.

Many high-impact companies are already leading the way. Of the 166 companies assessed here, more than 70% have now disclosed some form of high-quality target to CDP or had one approved by the SBTi.

That’s good progress, but the focus is too much on Scope 1 and 2. And targets are just the starting point. More than two years into the ‘decade of ambition’, we urgently need to see not only targets, but clear transition plans and evidence of real reductions taking place.

Financial institutions play a critical role. They should directly ask the highest-emitting companies to set high-quality targets, for example by joining the 2022 CDP Science-Based Targets campaign, and urge them to develop credible transition plans.

Meanwhile, the CDP temperature ratings dataset used for this analysis is available for use by financial institutions to analyse their portfolios, compare the quality of corporate targets, and set their own emissions reductions goals to reduce their financed emissions to fulfil their net-zero or Glasgow Financial Alliance for Net-Zero (GFANZ) commitments.

Click to see Chart 1, Chart 2 and Chart 3.

{kind=link}

{kind=link}

{kind=link}

[1] This analysis was available for 88% of the companies with a target.

[2] This analysis did not account for double-counting of GHG emissions. Data: https://publications.jrc.ec.europa.eu/repository

[3] For the analysis, companies without a valid target were assigned a default temperature score of 3.2 °C.